In our most recent article, we arrived back at the question, what is in an ESG fund name? as funds with an ESG label in the name continued to outsell their non-named peers across Europe. A question first posed in our insight, Act I: To ESG or not? That is probably not the question.

We have therefore turned our attention to this question, leveraging Simfund’s recently expanded ESG data set. To answer this question, we analysed the 200 best-selling ESG named Article 8 funds of 2022 on the basis of six ESG characteristics and measured them up against the broader Article 6 and 8 universes.

For more detail on the 200 best-selling Article 8 and ESG named funds examined, see The what’s what of the 200 section at the end of the insight.

Rise of the 200

In making our comparison of the 200 best-selling Article 8 ESG named funds to the rest of the Article 8 and 6 universes, one thing is clear: The 200 on average outrank the rest on nearly all ESG measures examined. And the rest of our Article 8 universe on average outranks the Article 6 universe on all observed criteria. Our headline results therefore fit what most will have expected and/or wanted to observe. Funds purporting to be greener—or at least those more forward on marketing their ESG credentials—are on average greener. The points of most significant difference between the universes, exclusions and weighted-carbon intensity also do not surprise. Regarding the former, exclusions are one of the oldest ESG investment policy measures to be used. Regarding the latter, environmental issues tend to top the ESG agenda for many investors, with climate being issue number one.

Notes: When considering the information below, please note that a lower measure is better for ESG Governance Quality Score (measures governance risk), NBR % Holdings Red/Amber and ESG Weighted- Carbon Intensity. Emerging market (EM) and money market funds have been removed. EM funds were removed as in general these funds’ ESG credentials were noticeably poorer than the rest of the sample.

Figure 1: Comparison of select ESG measures

Source: Simfund, Global. Data as of December 2022. Money market and emerging market funds excluded.

Averages, however, can conceal much within a sample, and cannot answer the question of, and in keeping with Shakespeare’s Juliet, Does a rose by any other name smell as sweet? Or more specifically, would a fund containing no-ESG terminology in the name but with similar characteristics to the 200 best-selling funds be as attractive to investors?

Are there any other roses out there?

In our search among the rest of our Article 8 and Article 6 universes, whereby we looked for funds that met or exceeded four of the six benchmarks (including having at least one exclusion) set by our 200 best-selling funds, 2,237 additional funds were found. Of these, 1,655 were Article 8 (1,101 without an ESG term in the name) and 582 Article 6 funds. This highlights that although the 200 best-selling funds on average demonstrated superior ESG credentials, these ESG metrics are not unique to only the 200 best-selling data set. The 200 best-selling funds, however, massively outsold these additional 2,237 funds in 2022, registering an estimated $100 billion in inflows compared to nearly $40 billion in outflows for the other funds. On ESG characteristics alone then, it does not appear that a fund by any other name will be as attractive.

Figure 2: The other roses

Source: Simfund, Global.

What is in an ESG fund name?

We are therefore left with the impression that investors consider an ESG labelled fund to be more than the sum of its ESG characteristics. Afterall, having above average ESG characteristics says nothing about the investment process. Nothing prevents an Article 6 fund from having above average ESG metrics; it simply is not a key objective of the fund. Our results therefore point to the fact that language matters here. And it might just be that ESG named funds, particularly those with above average ESG credentials, outsold their competitors because investors include naming conventions and other language used throughout supporting documents as part of their filtering process. As investors are not investing for today but for tomorrow, they must naturally look for supporting evidence, often qualitative, that a fund’s current ESG positioning could carry forward. Past performance does not guarantee future results.

What is in an ESG name? For investors, an expectation. An expectation that the fund will meet its ESG objectives, which in many cases will mean being ahead of the curve on ESG. In naming ESG funds, fund managers therefore need to consider the risk and rewards of setting investor expectations. For with great expectations comes great risk. Meet lofty expectations and you have a winning narrative; fall short of expectations, and risk your reputation, particularly in today’s scrutinous environment.

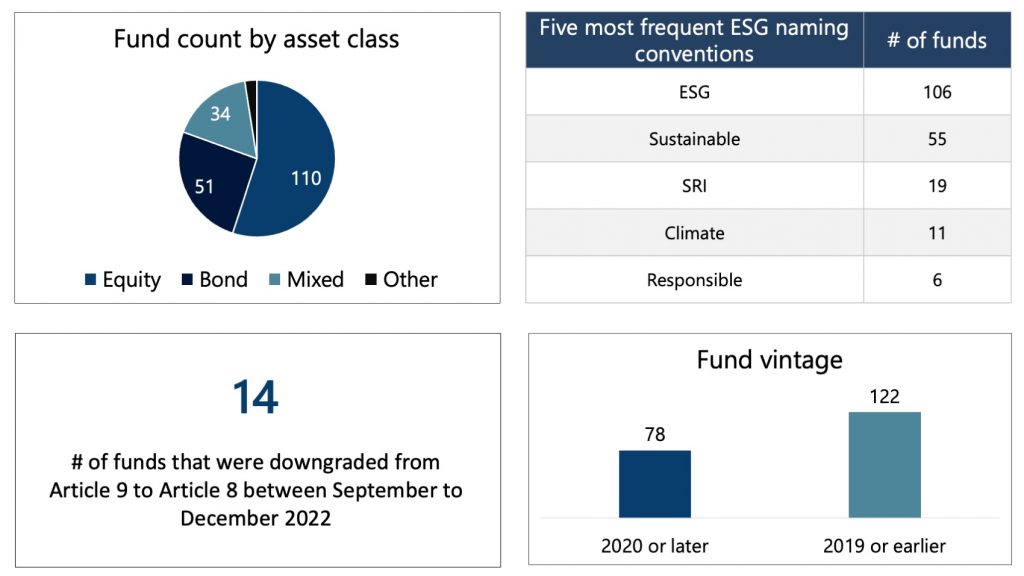

The what’s what of the 200

The charts below summarize the funds contained within the 200 best-selling Article 8 ESG named funds. An analysis of the sample with and without EM funds is also presented.

Figure 3: 200 best-selling Article 8 ESG named funds

Figure 4: ESG credentials of the 200 best-selling ESG named funds

Talk to us today to learn more about how ISS Market Intelligence can help your business.

Commentary by ISS Market Intelligence

By: Benjamin Reed-Hurwitz, Vice President, EMEA Research Leader, ISS Market Intelligence.