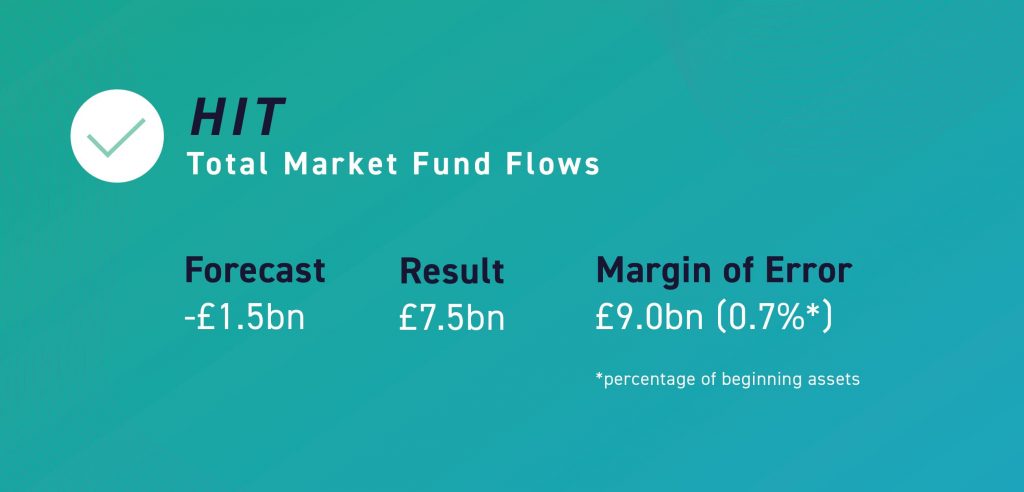

Our January insight, The Hangover, predicted that economic uncertainty, particularly at the household level, would continue to cast a shadow across the UK-domiciled fund industry—a prediction that has largely played out. All hope was not lost, however. While 2022 ended and 2023 began with winds of caution, as estimated net flows crossed 0.1% just once between December to April, the month of May brought winds of hope, with net flows of close to 0.3% of beginning assets. With May’s positive net flows, our previous forecast, generated using ISS Market Intelligence’s analytical tool supreme Flowspring in combination with the Simfund data platform, turned out to be overly pessimistic. Organic net flows for November to May came in higher by 0.7% of beginning assets.

Figure 1: UK-Domiciled Fund Forecast Result

Key takeaways from the past six months

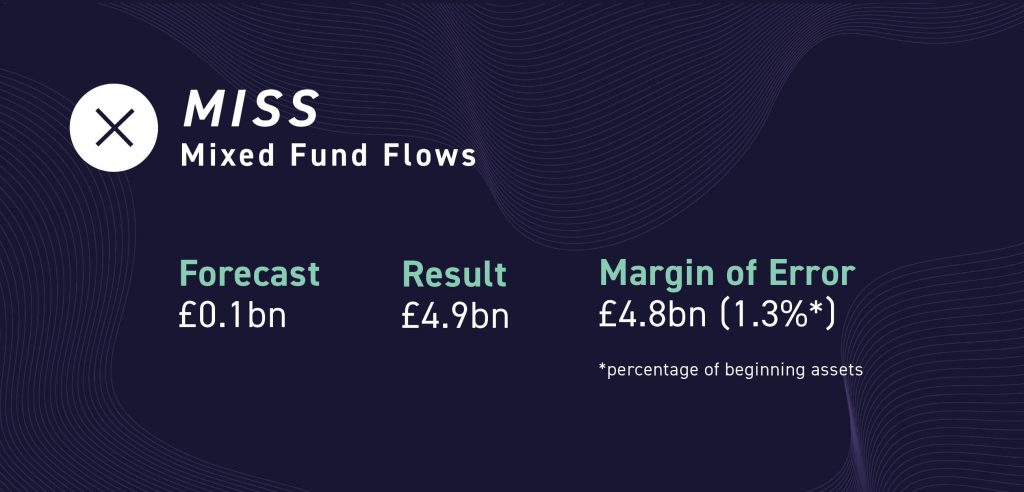

Nothing mixed about these results

Six months removed and our comments about mixed funds in the previous edition of Hit or Miss still apply. Mixed funds remain a bedrock of the UK retail fund distribution business—a fact that will likely be further bolstered by the Financial Conduct Authority’s Consumer Duty rules, continued consolidation activity amongst fund distributors and shifts by financial planning and wealth management firms toward centralized investment propositions.

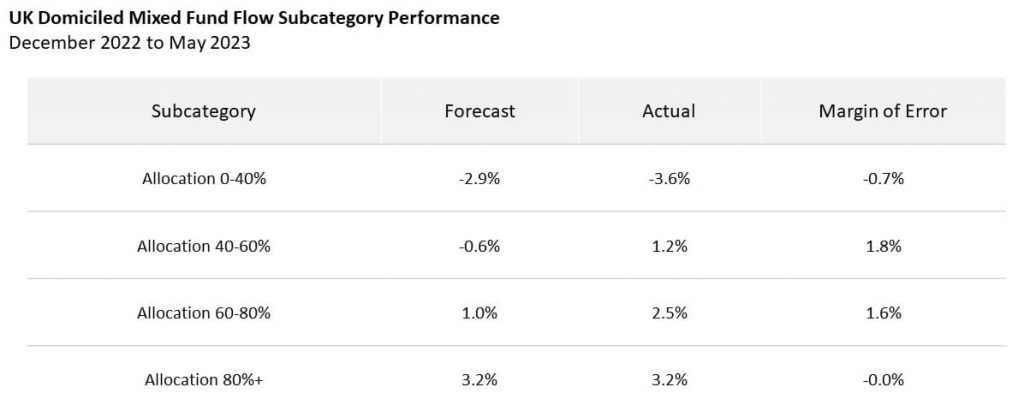

Once again, mixed funds led the way again in terms of net flows in the trailing six months to May 2023. Our forecast, however, did not see this coming. Opposed to a realized six-month organic growth rate of 1.3%, our January forecast saw mixed funds only breaking even throughout this period. While the model accurately predicted, almost to a tee, the flows into mixed funds with an equity allocation of 80%+, the biggest miss was on funds with an equity allocation of between 40-80%. This miss is likely related to the fact that rises in interest rates have impacted the relative attractiveness of bond and equity investments, with bonds becoming more in favour; mixed funds with a lower gearing of equity may therefore find renewed interest.

UK equity just cannot catch a break

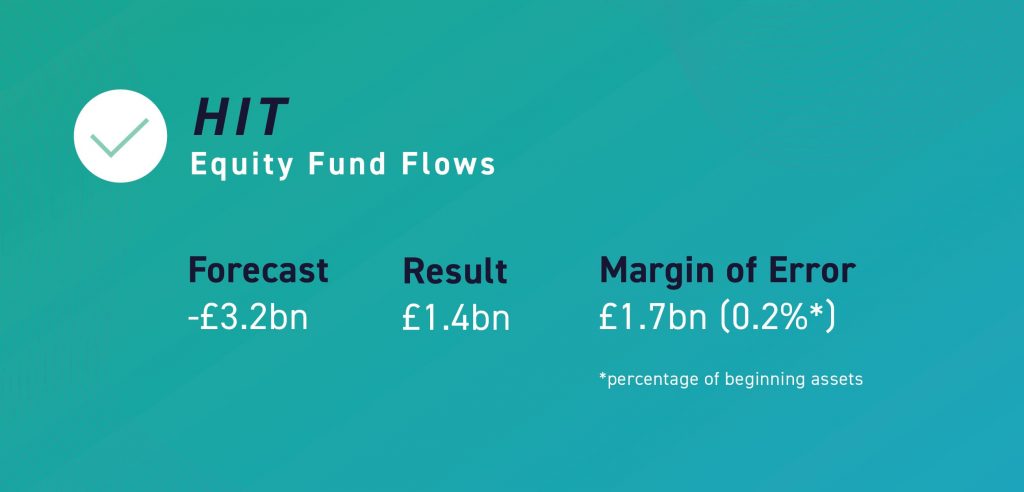

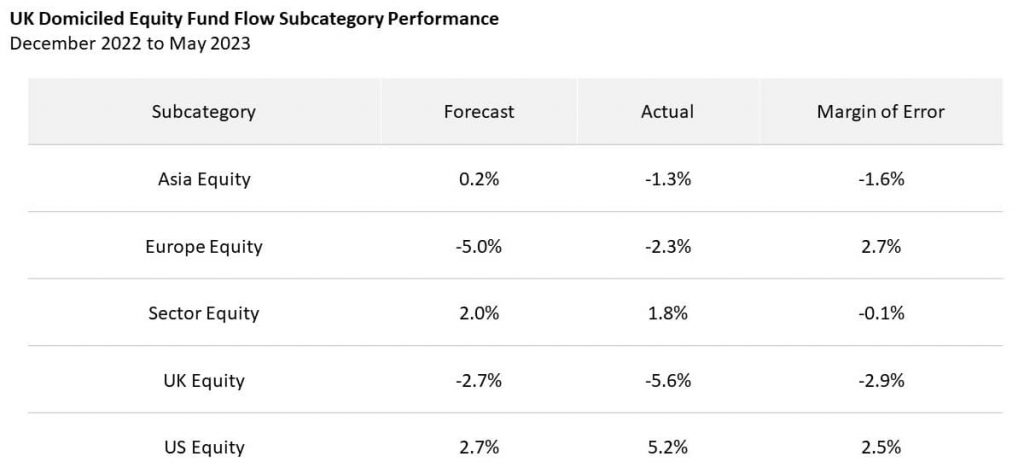

The equity fund prediction for organic fund flows appeared to be prescient, missing by a mere 0.2% of beginning assets. It did, however, underestimate just how bad the UK equity picture would be. The decline of UK equity was another topic surmised on in our past Hit or Miss insight. Investors in the UK continue to search for opportunities abroad. And with anemic performance amongst the FTSE 100, it is hard to fault investors. Until there is a discernible turnaround in the performance of UK equities, there are no signs that these clouds will dissipate. Meanwhile, while European funds may have not taken the expected wallop, they nonetheless continued to see significant outflows. With political uncertainty continuing to reign in the region, expect investors to continue to make their equity selections amongst Global, US and Asian strategies. US and global equity funds were expected to lead the way from a sub-category perspective in terms of absolute organic growth—and did so by an even greater margin than forecasted. Indeed, home bias amongst UK investors is increasingly becoming “flat-sized.”

Bo(u)nd for success

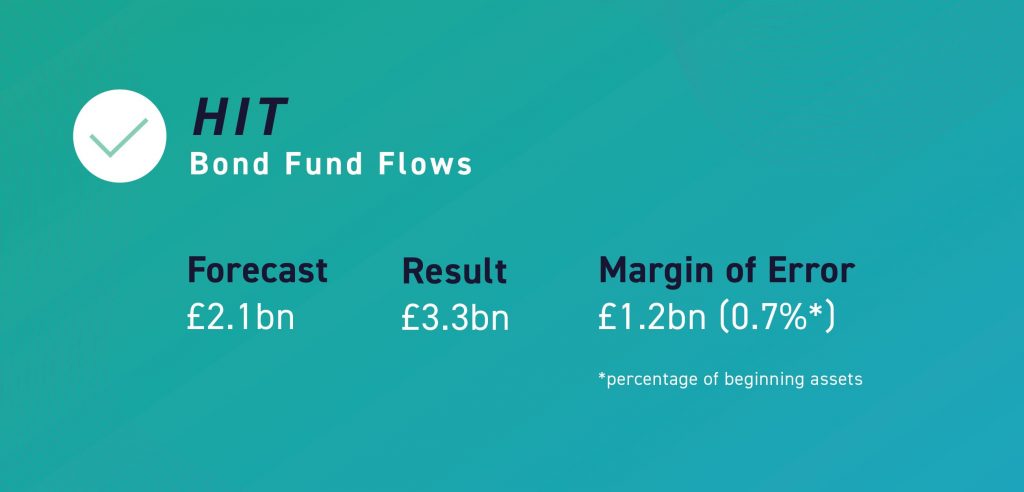

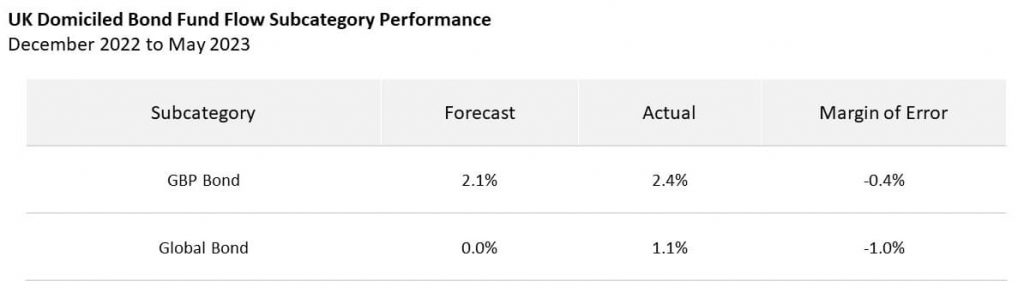

With rates having substantially risen and the economic picture remaining cloudy, bond funds had been predicted to do well, which is largely what happened. Bond funds, led by GBP bond fund categories, posted the second highest six-month organic growth rate at 1.8%. While recent interest rate rises have taken a bite out of bond prices, it has now put bonds in the enviable position of offering up the potential for both yield and capital appreciation. The former being something that, to put it lightly, has been in demand for some time. Today’s bond demand in fact feels downright nostalgic; it certainly has been a while since rates were this high. Uneven global equity markets have only added to the case for a more conservative shift in investors’ portfolio allocations. How far the shift goes, is anyone’s guess.

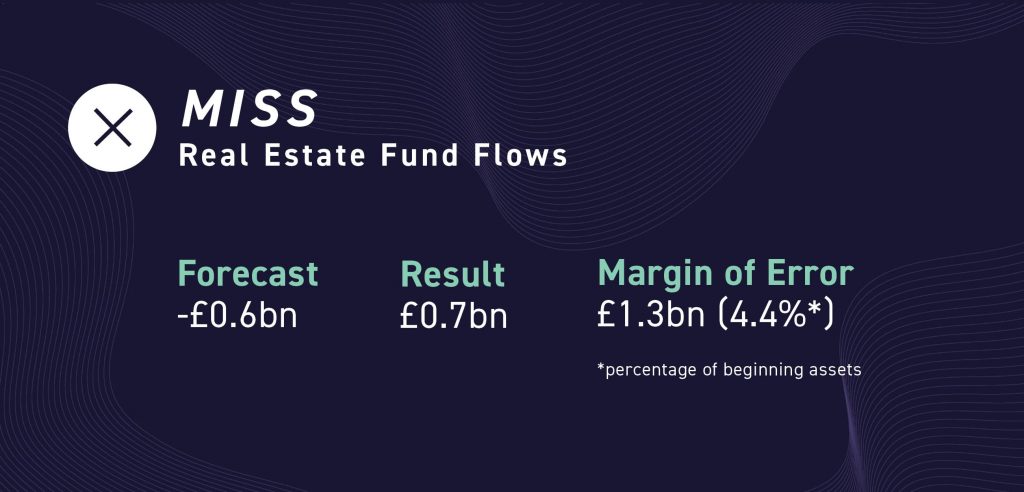

Is that growth for Real (Estate)?

The Real Estate fund category had been expected to perform the worst, on an organic growth basis, of the asset classes forecasted. With Direct UK Property funds still stuck in paralysis due to liquidity concerns, both actual as well as related to the potential for regulatory action on this front, prospects appeared slim for a turnaround in the asset class’s fortunes. This turned out to not to be the case. Instead, Real Estate Funds registered the greatest relative organic growth at 2.5%. The growth, however, was driven entirely by two funds.

One major contributor, the iShares Environmental and Low Carbon Tilt Real Estate Index Fund, has seen previous success in terms of attracting flows. The other contributor, the Aviva Investors Real Estate Active LTAF, speaks to a brand-new opportunity in the UK. The Long-term Alternative Fund (LTAF) product structure was introduced by the FCA in 2021 and allows investors to access illiquid assets through an open-ended authorized fund structure which has additional controls around the flow of investor money into and out of the fund. Due to the more complex design, distribution has initially been restricted, but is now set to expand to include retail investors.[1] The introduction of the LTAF therefore breathes new life into the illiquid investment arena, with direct property being one asset that may benefit. It may also herald the end of the Property Authorised Investment Fund (PAIF)—a vehicle that has been most recently challenged by liquidity events during and post-pandemic. If the PAIF does find itself relegated to the annals of history, let us leave it to the historians to judge the success of this vehicle.

The churning

A tale in Indian mythology goes like this: The ocean was once churned by positive and negative forces, and the activity resulted in retrieving back lost wealth from the depths of the ocean. In a cyclical business, such as the fund business, the idea of wealth “churning” seems apt. While those fund managers experiencing significant asset declines over the past six months due to flows and performance may be particularly heartened by the idea of lost wealth being resurfaced; they should not rest easy. Although investor money that fled to the sidelines in 2022 will likely resurface, there is no guarantee that it will return to its original keepers. The question is then: Do you know where tomorrow’s wealth will resurface? And what it will take to capture it again?

Talk to us today to learn more about how ISS Market Intelligence can help your business.

Notes:

[1] For more information, see: https://www.fca.org.uk/publications/policy-statements/ps23-7-broadening-retail-access-long-term-asset-fund

Commentary by ISS Market Intelligence

By: Benjamin Reed-Hurwitz, Vice President, EMEA Research Leader, ISS Market Intelligence.